Still downloading templates?

There’s an easier way. Try a free AI Agent in ClickUp that actually does the work for you—set up in minutes, save hours every week.

Sorry, there were no results found for “”

Sorry, there were no results found for “”

Sorry, there were no results found for “”

Just because the cash register is ringing doesn’t mean every project is a rockstar. The financial performance of a project is not just about the revenue numbers. You have to factor in elements like budget used, completion time, and the relative benefits derived for measuring success.

Now, the million-dollar question: How do you sift through the winners and losers efficiently? By implementing a balanced project accounting system, of course.

Picture this: questionable revenue, budget gone rogue, and no tangible track record of actual costs—that’s nightmare stuff for project accountants and project managers alike. Project accounting focuses on turning these financial woes into financial whoa by bringing order to everyday revenue operations! 🥳

We’re here to break down project-based accounting and show you how it can be a game-changer for your business. No fancy jargon—just straightforward insights into:

You may be familiar with general financial accounting, but project accounting is a different beast. In simple terms, it’s about tracking project financials at any scale to measure the profitability of a job. You get to track cost centers and profits for individual projects in your company.

Unlike general accounting, which provides an overview of a company’s overall financial position, project accounting drills into the specifics of each project’s financial health. Its microscopic overview lets you see the intricate details that might otherwise be lost in the broader landscape of your financial statements. 🔬

As a business owner, you’re always looking for methods to increase project profitability, and project accounting enables just that. By keeping track of each project’s expenditures and income, you determine which initiatives are the most lucrative and which should be reviewed, refined, or even abandoned.

Plus, with a granular understanding of how money is spent and earned on each project, you anticipate potential cash flow issues faster, plan resource management more effectively, and make informed decisions about future projects.

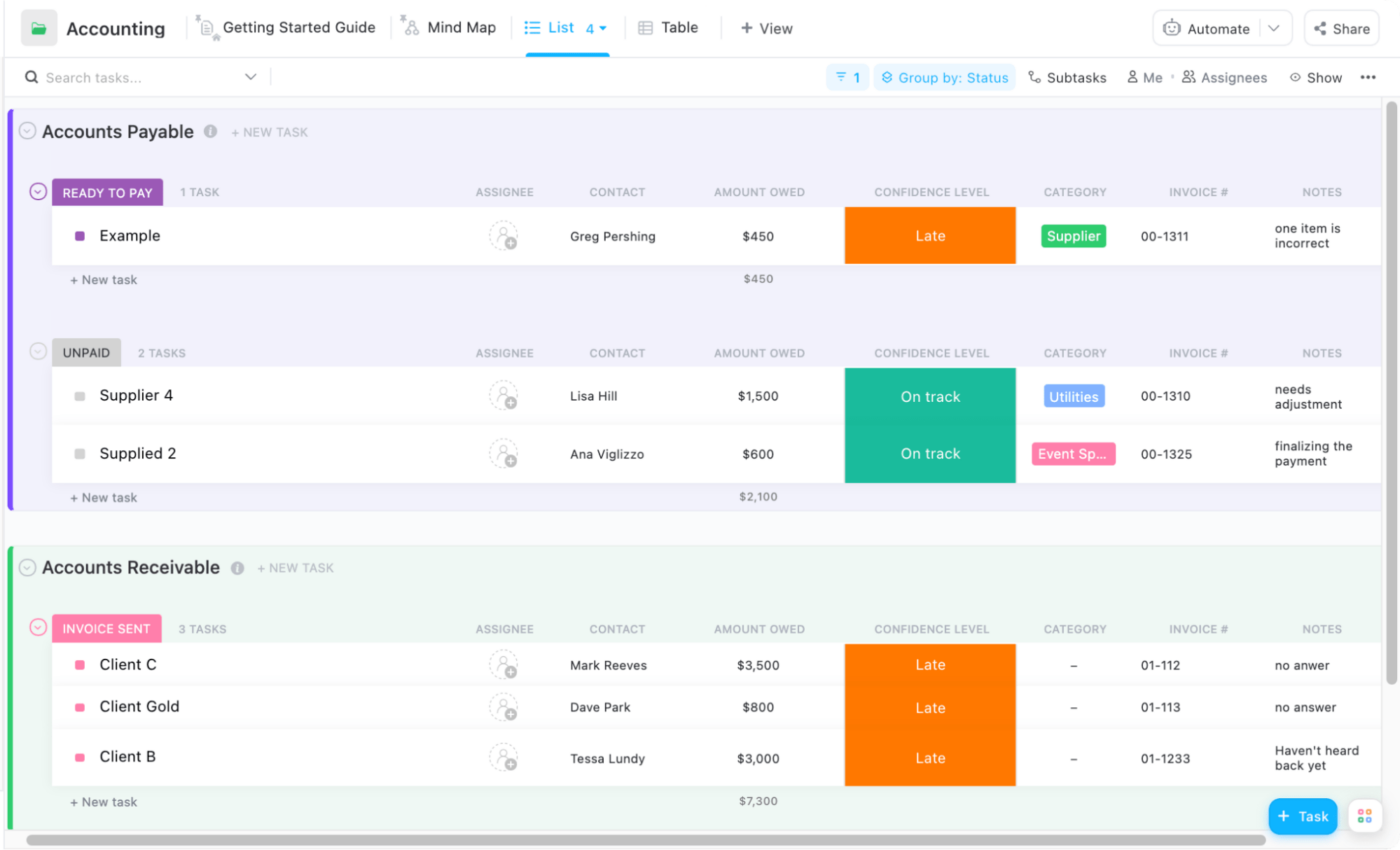

Bonus Tip: You can now use ClickUp to manage Project Finances to get full insights into the profitability of your ventures. From tracking your project budget to managing payment deadlines, handle everything from a single platform. 🤠

By grasping carefully vetted project accounting principles, you can ensure a smoother workflow and better financial management for your portfolio. Here are the five major principles to stick to:

Still considering the reasons for adopting project accounting? Here are four top benefits that become accessible upon implementation.

Project accounting allows tracking both per-day and cumulative project costs for specific hierarchies across departments and cost centers. With a real-time financial radar for every outflow, it’s incredibly simple to make intelligent resource allocation and other managerial decisions and stay one step ahead of possible hurdles.

Project accounting helps identify potential cost savings and allows managers to make on-the-go adjustments to project budgets, ensuring efficient resource management.

Budgeted data and comparison with actual figures also help you make more accurate fiscal projections, as well as bid with robust estimates for future projects. And when it comes to pricing your products and services, project accounting is your cheat code to staying competitive and profitable without going overboard on the spending. 💸

You can generate comprehensive financial reports for each project, offering stakeholders—who may not always understand the complexities of project accounting work—a crystal-clear view of project performance. The reports are typically comparative, allowing for tracking fiscal differences and locating savings potential meaningfully.

This level of transparency strengthens your professional relationships, particularly with clients, and elevates your reputation as a reliable and trustworthy business entity. It’s a strategic move that goes beyond numbers, demonstrating your commitment to financial integrity. 🌼

Project accounting is your ticket to controlled financial transactions and billing logistics. It steps up to keep you in the loop, always up to date about, say, material orders or payment deadlines. Everything runs like clockwork, and there’s a significantly lower risk of the project getting derailed.

Investing time and resources in project accounting and implementing it meticulously will pay you back multifold. Plus, it’s your guide to figuring out which clients and projects are the real winners or what process inefficiencies are costing you big time. The only problem for most project managers is: Where do I start?

We have broken down the standard project accounting cycle into seven steps. Read along, put them to the test, and see firsthand how the right project accounting process flow can transform the way you manage project finances. 🔥

The initial step, and perhaps the most crucial one, is to establish a solid foundation by defining your project accounting needs. Think of it as the cornerstone of a building—without it, the structure might not stand the test of time.

Get the project team together for this exercise, including key people like the project manager, project accountant, and department heads. Collectively, you can:

💜Bonus: Use ClickUp’s free Year-Over-Year Growth Calculator to calculate year-over-year revenue growth and identify whether your projects are truly scaling profitably.

If you’re looking for project management software with built-in features for handling project accounting and auditing tasks, you can consider ClickUp. From setting measurable project Goals to allocating resources within time, people, and budget constraints—it’s a one-stop solution with accounting tools perfect for both new and experienced project managers!

Since this step focuses on creating a project outline, why not start with the ClickUp Accounting Project Proposal Template? This template is your go-to guide for laying out the whats, whens, and hows of a particular project. It helps you spell out exactly what ROI or profit margin you’re aiming to achieve and establish project accounting rules. ✍️

Once you’ve nailed down your project accounting needs, it’s time to prepare a suitable plan that aligns with them. The idea is to align your project accounting systems with your business’s overall financial accounting framework. Answer questions about tax and legal repercussions, fiscal overlaps, and contingency funds.

Start financial planning for projects the right way using the ClickUp Accounting Suite. It comes with 1,000+ templates suitable for accounting and project teams. 😍

For instance, if you want to collaborate with team members on your accounting plan, just jump on the ClickUp Accounting Operations Template. Its ready-made structure can be used to organize and track operations within individual projects, making it easy to centralize your accounting tasks.

Other benefits of ClickUp include:

While investing in good software is vital, it’s got to match your wallet size. Luckily, this project management software is like a pair of stretchy pants—it grows with you! And the best part is that it comes with free, pocket-friendly, and customizable enterprise plans.

Believe it or not, accurate budgeting and cost estimation form the bedrock of efficient project management, ensuring your project stays financially viable and sustainable. Here’s how you can do it:

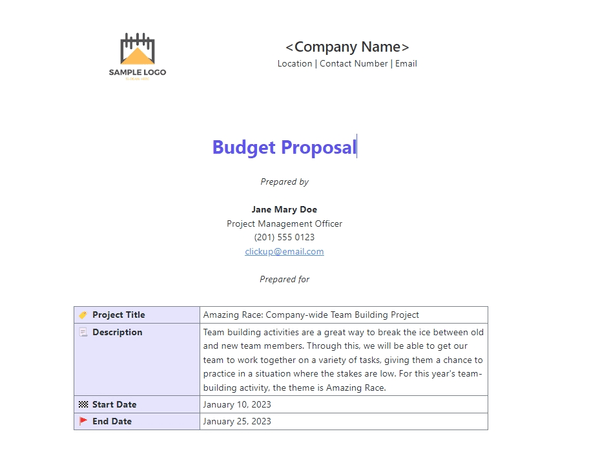

Easier said than done, but we’ve got you covered with the “done’’ part, too. The ClickUp Budget Proposal Template acts like your financial GPS. It breaks down project costs into bite-sized pieces, ensuring you and your stakeholders have a reliable financial roadmap. 🛣️

Not all company projects bring in money right away. Some projects, like simplifying a time-card system, don’t even make money directly, but they set the stage for a wider profit margin in the future. On the flip side, projects such as building a house, constructing a road, or creating a new software product can generate revenue that covers their costs within a defined timeline.

When it comes to getting paid for projects, the revenue recognition varies—and your project accounting system must adapt to that. Some projects pay once the work is done, while others follow the cost-to-cost method and register partial payments as the work progresses.

It’s smart to set clear rules on when you get paid and when you actually count that money as revenue—do this before kicking off the project. 💲

You can track the revenue and growth for individual projects with the ClickUp Revenue Growth KPI Tracking Template. Create copies of this template and customize it with unique revenue recognition styles and performance benchmarks.

Why should you implement real-time expense and time tracking? Easy: to ensure everything stays on budget and schedule. You will be able to identify any unforeseen expenses or delays as soon as they appear, allowing you to take quick action for project success.

You may want to use ClickUp Project Time Tracking to track labor hours, segregated timesheets, and expenses and get an up-to-the-minute snapshot of project progress. ⏳

For an even quicker way to keep tabs on your expenses, check out the ClickUp Project Cost Management Template. Let’s say you’re handling project cost accounting for a construction venture. This template makes tracking project costs for different things like materials, labor, permits, and equipment effortless. See how your budget holds up in real time and update in the event of price spikes and similar changes.

Project accounting is much like management accounting: you must understand what numbers represent and how they impact project success. With native reporting options within ClickUp, it’s easier to get numerical and visual reports for different project parameters, including team resources and budget trails. Use these insights to enhance your project accounting practices, improve efficiency, and increase profitability. 💯

Two additional tips:

Need a go-to? The ClickUp Project Reporting Template lets a project manager zoom in on those areas needing a bit more love by painting a detailed picture of high-level KPIs and overall performance. It helps you keep tabs on crucial elements like project tasks, expenses, and lingering to-do items.

Don’t just sit on compiled data; analyze it right away. Use it to identify trends, forecast outcomes, and identify completion risks. Keep an eye out for any potential issues that could derail project finances. These could range from cost overruns and delayed timelines to unanticipated resource allocation needs.

Let’s say some of these scenarios came true. How would you handle them? Well, ClickUp can level up your issue management game with:

Be proactive here, as swift corrective action can mitigate any adverse impact on project profitability.

Project accounting best practices revolve around effective project management processes, controls, and procedures when addressing issues. There are some best practices you can follow while making decisions around pricing, bidding, contract processes, and contract provisions. The goal is to improve the development of controls and documentation.

Here are some key best practices to follow:

For project accounting within engineering firms, maintain a detailed SOV outlining the cost for different work portions in a completed contract. This enables a transparent percentage of completion calculation.

Regularly review meeting minutes and progress reports to detect deviations from the original agreement and alert your accounting team accordingly.

Keep a consistent check on project reporting, especially the cost reports, to ensure there are no unsupported financial transactions. Use Request for Information (RFI) documents to address information gaps in plans, contracts, documents, or specifications when necessary.

Change orders signaling alterations to the original statement of work can confuse the entire team and lead to project budget disruptions and halted work. Develop a change order plan to allow project managers to tweak every cost center carefully.

Regularly review labor hour documentation, potentially every week, to align with the project forecast. Verify that all subcontractor bills are for approved charges.

Recalculate the project schedule regularly, starting from the task level and progressing to the overall project and macro (company-wide) level, ensuring timelines align with expectations.

Implementing project accounting is a must for service-based businesses to thrive. It fosters transparency, offering project managers the necessary insights for optimizing financial performance and achieving long-term project success.

Project accounting software, distinct from traditional financial accounting systems, stands as a proven method for service organizations to enhance resource utilization.

Both accountants and project managers juggle a variety of tasks, often using a bunch of separate tools. But by signing up for ClickUp, you can manage everything seamlessly on a single, comprehensive project management platform! 😎

© 2026 ClickUp

There’s an easier way. Try a free AI Agent in ClickUp that actually does the work for you—set up in minutes, save hours every week.