10 Effective Tips to Manage Project Cost Risks

Sorry, there were no results found for “”

Sorry, there were no results found for “”

Sorry, there were no results found for “”

Ed Naughton is the Chairman and Founder of the Institute of Project Management, the former Vice President of the International Project Management Association (IPMA), and an internationally respected expert in the discipline.

Visit the PM World Library and International Project Management Association for his published work.

Did you know that up to 35% of projects fail to meet business objectives of stakeholder satisfaction?

The success of a project often depends on your approach to risk management, mainly how you deal with project cost risk.

So, out of all the successful projects, only 62% manage to stay within budget. Exceeding the project’s planned budget, otherwise known as cost overrun, is one of the most common risks.

To avoid that from happening, every project should have its risk management plan. Risk analysis and management are essential to ensure your project runs smoothly with the fewest possible surprises.

Although risks are not something that can ever be fully managed, having a proper plan for their occurrence is crucial if you want to avoid your project becoming a failure.

Cost risk is one of the most common project risks. It can arise from poor budget planning and inaccurate cost estimation. Cost risk is the risk of exceeding the budget for a project or failing to deliver fair value to offset costs. In addition, you may face higher costs due to internal or external factors. But what exactly are those?

Internal risks occur due to inner actions within the business. For example, underestimating the amount of work needed for a project is likely to result in an extended schedule, which adds to the project’s cost. The longer the project is, the more it costs. It’s obvious! That also means this risk is related to not only schedule but also performance and quality.

The good thing about internal risks is that you can avoid them with adequate planning and project management. On the other hand, external cost risks are often out of your control.

External cost risks include risks that occur outside of the business. That may include changes to regulations or industry standards, or banking charges. Although you can’t control these issues, you can mitigate their impact on your project.

The biggest problem with these risks is that you can’t predict their likelihood of occurrence. Sub-groups of external cost risks include economic, political, and natural risks.

There are a variety of causes of failure, but most of the issues are linked to poor cost management. Simply put, if you fail to keep costs under control, your project fails. With cost risk management, you can foresee future expenses. That budget visibility is a neat thing to have because it allows you to make decisions that will steer you away from debt.

According to PMI’s 2021 study, 38% of projects don’t stay within their planned budget range and 35% of projects fail because of a budget loss.

Cost risk management is a crucial part of managing a project as often the project’s success or unsuccessful outcome depends on it.

Use the following tips to manage project cost risks better and increase your chances of success.

Although you may not be able to control all the risks involved in your project, you should prepare for them as much as you can, especially for those you can control. Here are a few things to keep in mind when trying to manage project cost risks:

Project costs are typically divided into three basic groups:

*Direct costs are often the source of cost risks out of these categories. Therefore, it’s essential to pay attention to the cost of labor, equipment, and materials to help decrease the risk of ballooning costs.

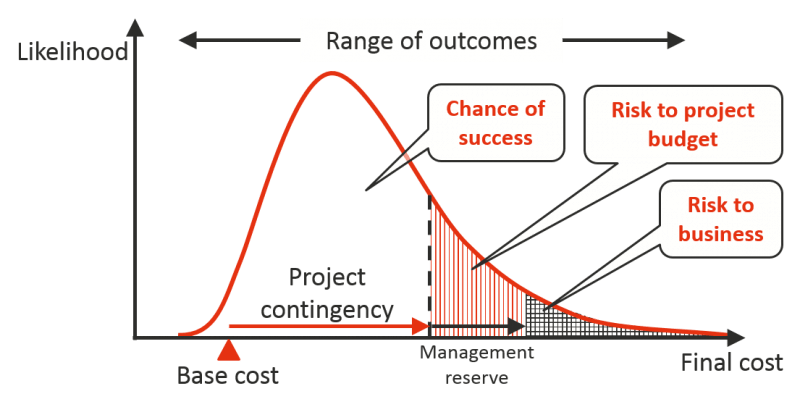

A contingency is a future circumstance that you cannot guarantee will or won’t happen. For example, you can’t guarantee that your project will finish on time, which increases the cost of labor and overhead.

Including contingencies in your project budget minimizes the impact of these events on your bottom line. In addition, setting aside a portion of the budget helps you deal with unforeseen costs.

Consider setting aside an even larger chunk of your budget for projects with increased risks.

A successful project needs a detailed roadmap. A roadmap provides an overview of the project’s timelines and objectives. As part of your roadmap, you’ll need to identify possible risks.

Risk management planning helps you identify, evaluate, and mitigate potential risks. It also requires you to define your risk tolerance; you can set thresholds for the level of risk you’re willing to take.

Risk tolerance makes it easier to prioritize risks. You can decide which issues require immediate attention and which can lead to better decision-making and lower costs in the long run.

A risk management plan should also include a response plan. First, decide how you deal with specific events, such as going over your labor budget or spending more on materials than anticipated.

As part of your risk management plan, create a risk register. A risk register provides a list of all the risks that you identify during the project assessment. It gives you a blueprint for anticipating and resolving issues quickly.

Include a variety of fields for logging each risk. For example, describe the risk, the anticipated impact on the project, and how you plan to respond if it occurs. You may also want to assign someone to each risk instead of making tracking risks the responsibility of a sole team member.

Continue to monitor risks throughout each stage of the project. Keep track of the status of the risks, so you know when to initiate your response plan.

Your risk register should include the likelihood and impact of each risk. The likelihood of a specific risk is the probability that it’ll occur at some point during the project.

For example, the risk of delays due to a shortage of materials from vendors or suppliers may increase during supply chain issues. You may also face a higher likelihood of slowdowns when dealing with a lack of labor or resources.

After analyzing the likelihood of an event, you’ll need to consider its impact. Think of how the event may disrupt your plans, requiring you to halt other work or delay a stage of the project.

You can also rate the likelihood and impact of each event on a numerical scale of one to five or one to ten. Ratings help you prioritize your resources when dealing with risks.

Bonus: Use RAID templates to manage risks!

Cost estimating is the process of forecasting the cost of the project for achieving specific goals. The cost estimation should account for every element needed for the project, including labor and materials.

A work breakdown structure (WBS) helps you create a more accurate cost estimation. It requires you to divide your project into smaller, more manageable tasks.

A WBS is also a common tool for deliverable-based projects. You can separate the project into smaller work packages (WPs). Each WP should have its own costs, risks, and assigned team members. A work package makes it easier to detect cost overrun in a specific task before it starts impacting other areas of the project.

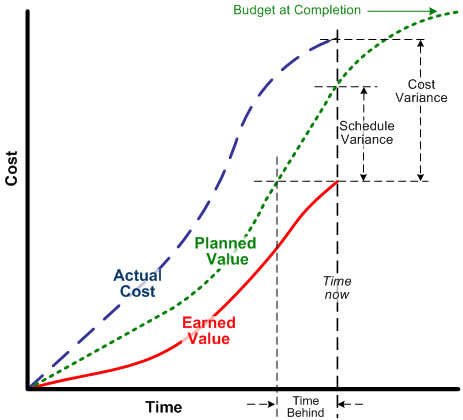

Earned value management (EVM) helps you measure the performance of each task or work package. It involves assessing current performance against planned performance.

This technique can help you manage and control your project, but you can’t rely only on EVM because it can quickly change.

If you measure all your risks with EVM, you can cover the impact of one or more risks occurring with the contingency budget.

Earned value is the amount of the budget that you’ve earned based on the amount of work completed.

Let’s give an example: the project budget is $20,000 with a timeline of six months. After three months, you’ve completed 50% of the work. The current earned value is $10,000. At this stage of the project, you should’ve spent about half of the budget.

When the actual costs start to exceed the earned value, you need to stop and assess the cause of the cost overrun.

Finding the right vendors and suppliers for the project can help mitigate project cost risks. Delays and increased charges from vendors and suppliers can impact the cost of your project in multiple ways.

When comparing vendors and suppliers, pay attention to more than just the prices. You also need to ensure that your partners are reliable and capable of delivering goods or services on time.

For example, if a vendor can’t fulfill an order, you may need to use different equipment, materials, or software to complete a task. These changes can add to your costs and schedule.

Altering the scope of a project often leads to increased costs. Clients and stakeholders may propose changes to the project at any point. However, some changes may drastically add to the costs or timetable for completion.

Project managers need to know which changes are too difficult to implement without additional funds. Sticking to the planned scope of the project helps keep the budget and schedule on track.

Learn about the project management triangle and see how costs, scope, and time impact a projects quality.

Check out these budget proposal templates!

Never stop looking for unexpected costs. Instead, frequently monitor your progress using the best tools available, such as project management software.

Project management platforms, such as ClickUp, provide a customizable solution for tracking every area of your project. For example, if you’re feeling overwhelmed with project risk management, ClickUp’s budget template can be handy for tracking your project budget and helping you keep an eye out for cost risks. In addition, you can easily manage workflows, set goals, and view real-time statistics with ClickUp’s visual dashboard.

These are just a few of the advantages of project management software. You can also save time, improve communication, and much more.

Cost risk management is essential for the success of your next project. Pay close attention to all related costs throughout each stage of the project.

You’ve got the most control over direct costs, including the costs of equipment, materials, and labor. To better prepare for risk events and gain greater control over project cost risks, consider using project management software.

An effective project management solution like ClickUp can prevent overscheduling and mitigate other risk factors associated with cost increases. Use it to stay organized, manage your budgets, get real-time reports, communicate with your team, and so much more.

PMO Team

Max 9min read

Praburam Srinivasan

Max 22min read

Praburam Srinivasan

Max 24min read

© 2026 ClickUp