Sorry, there were no results found for “”

Sorry, there were no results found for “”

Sorry, there were no results found for “”

Have you ever wondered why your wallet sometimes seems to have a mind of its own?

That is precisely what Morgan Housel explores in his book The Psychology of Money. He establishes that how you handle your finances is linked to your psychological quirks and experiences.

Housel’s book isn’t just another finance book; it helps you understand why you make certain money decisions.

It provides valuable insights into the psychology of long-term investments and the very real human factors influencing investment decisions and money management approaches.

The book reveals the connection between money, emotions, biases, and uncertain long-term strategies.

Let’s look closer at Housel’s book and explore how managing finances isn’t just about numbers.

But before that, if you’re interested in reading more book summaries, check out and bookmark our curated collection of 25 Must-Read Productivity Book Summaries (including “The Psychology of Money”) in one place. You can save, edit, bookmark, and even export it for later use.

The Psychology of Money stands out from the crowd of personal finance books. Unlike books that claim to offer a universal path to wealth, this one takes a different approach.

Morgan Housel, a behavioral finance and investment history expert, is a renowned financial writer and analyst. In this book, he unveils a simple truth: financial success isn’t about raw intelligence but behavioral skills.

He emphasizes that your connection with money isn’t rooted in science or math but in emotions like fear and greed, pride and envy, and the social comparisons that shape your psychological relationship with money. Getting carried away by such emotions may make you less wealthy and keep you unsatisfied for life.

The book explores how our backgrounds and experiences make all the difference to our risk tolerance. For example, those who’ve seen the stock market rise in their formative years are likelier to invest money in stocks than those who have seen the market crash.

In the financial world, the concept of a “batting average” acknowledges that occasional losses are acceptable if overall gains outweigh them. When analyzing the Russell 3000 index, the author found that 40% of the companies on the index had failed.

However, 7% had performed well enough to offset this. These few companies contributed largely to the 73-fold increase that the Russell Index has seen since 1980. This highlights the importance of outliers.

In this book, Housel underscores the role of luck and risk in outcomes, the power of compounding, how you pay the price to make financial gains, and the tremendous influence of optimism and pessimism on decision-making.

The book challenges the conventional narrative, highlighting the importance of contentment in building wealth and having a happy and fulfilling life. It offers the valuable insight that true wealth lies in unseen financial assets.

The Psychology of Money provides a unique perspective in the crowded personal finance genre. Housel’s unconventional wisdom makes this read a standout, validating its widespread popularity.

Housel’s book is a short 20-chapter read that imparts enough wisdom for you to adopt a productive financial mindset. Some of its key takeaways include:

Housel believes that no matter how irrational your financial decisions may seem, you aren’t crazy. Your money habits come from your unique life experiences.

Your background and lived experiences influence how you manage money—your saving, investing, and spending habits.

In Western economies, people’s backgrounds changed as they shifted from hands-on jobs to more knowledge work. It changed how people approach finances, making old investment rules outdated. Different backgrounds lead to different money outlooks and risk preferences.

So, even if your financial choices seem weird to others, they make perfect sense to you. Your decision-making, including investment decisions, is based on what you know (and think) about the world.

You can build wealth even with a modest income, with the right financial decision-making. But without a high savings rate, it’s nearly impossible.

In his book, Housel stresses the link between good investing, saving a substantial portion of income, and adopting a humble, frugal lifestyle. You can increase your savings by resisting the urge to keep up with others.

Plus, the best thing about saving money is that it brings you options, flexibility, and the chance to wait for opportunities. It gives you time to think and the freedom to change your path on your terms.

Compound interest, or compounding, is the powerful force behind building your savings. Essentially, it’s the interest you earn on the interest over time.

In good investing, the key isn’t chasing the highest returns but earning consistently good investment returns over the longest time—a formula where compounding works its magic.

For example, Warren Buffett, an American businessman, investor, and philanthropist, is renowned for his investment prowess, financial knowledge, and immense wealth. What’s most remarkable about his journey is not that he had a net worth of $1 million by age 30, but that he accumulated $81.5 billion after age 60.

Buffett’s disciplined approach to consistent, long-term investing allowed him to unlock the power of compounding.

The message: opt for sustained, reasonable returns over big future risks.

Success and poverty are not solely the result of hard work or laziness; luck and risk play substantial roles.

When it comes to long-term financial planning, some factors are outside your control.

Using Bill Gates as an example, Housel illustrates the impact of luck. Gates’ success was influenced by luck, such as attending a high school with a computer (yes, these were a rarity back then), and risk, like his friend Evans dying in a mountaineering accident.

Recognizing the role of luck in success and risk in failure cultivates humility and compassion.

To achieve financial success, balancing risk-taking and optimism with humility, fear, and frugality is important. Recognize that your hard-earned money can disappear quickly and attribute some of your success to luck.

Survival, the ability to endure, is the cornerstone of financial strategy. Being financially unbreakable, allowing compounding to work wonders over time, becomes the goal.

A well-defined plan is essential, but it is equally important to plan for things not working out as planned. You should balance optimism with caution to achieve realistic optimism and pursue long-term goals.

Unknown risks are inevitable, and preparing for the unforeseen is challenging. Housel suggests avoiding single points of failure, like relying solely on a paycheck.

The biggest financial risk is neglecting savings, creating a gap between current and future expenses. Estimating future returns requires a margin of safety; for instance, the author assumes a one-third lower return than historical averages.

Prepare for the unpredictable nature of the economy. Ensure financial security by building sufficient savings to rely on.

Before you plan your finances, know if you’re a long-term or short-term investor. Your time horizon and goals shape your perspective, influencing what prices seem reasonable.

Financial advice is not one-size-fits-all; commentators on the TV don’t know your priorities. Adopt a financial plan that aligns with your values and withstands short-term volatility. Aim for positive returns.

Build a portfolio that ensures good investment returns, quality of life, and resilience during economic challenges by acknowledging the human aspects overlooked by academic ideals.

Long-term planning of finances for both personal and business needs is challenging as your personal financial goals evolve with time. Your desires shift, and what matters today may not in a decade.

Accepting personal evolution is crucial in any investment strategy. Housel recommends keeping your financial plan flexible to adapt to your changing needs and priorities in life. Aim for moderation and invest wisely.

Housel reminds us that the final objective of financial planning and investing is to free up our time and give us the freedom to do what we want. By making wise financial decisions that build wealth, we gain control over our time and our lives. After all, success is just the ability to choose the life we want.

💡📚 Bonus: If you’re interested in reading more book summaries, check out our curated collection of 25 Must-Read Productivity Book Summaries in one place. You can save, edit, bookmark, and even export it from ClickUp Docs.

There’s no doubt that The Psychology of Money is filled with impactful insights about managing money, but some quotes stand out:

“Things that have never happened before happen all the time

This quote highlights the unpredictability of the future. In the world of finance and investments, market dynamics evolve constantly, leading to impactful occurrences. Remember the financial crisis of 2008? In situations like these, adaptability and long-term perspective help.

“Planning is important, but the most important part of every plan is to plan on the plan not going according to plan.”

While planning is crucial in financial decision-making, it’s also important to acknowledge and prepare for unforeseen events. Successful investing demands that you prepare to adjust the course when necessary. The most important part of planning is anticipating deviations to manage expectations and mitigate risks.

“Spending money to show people how much money you have is the fastest way to have less money.”

Spending money solely to display wealth for others’ validation is a waste of money. Instead, you can invest the money spent on such displays to gain genuine wealth.

“Luck and risk are both the reality that every outcome in life is guided by forces other than individual effort.”

Your life experiences may not always result from your actions alone. Luck and unpredictable risks also play a big role in shaping outcomes. So, it’s essential to stay humble, be adaptable, and make decisions with the understanding that not everything is within our control. Life’s a mix of effort, luck, and uncertainty.

“Your personal experiences with money make up maybe 0.00000001% of what’s happened in the world, but maybe 80% of how you think the world works.”

Our personal experiences with money, which are just a tiny fraction of global financial happenings, heavily shape how we see the world. It greatly influences how we make financial decisions and think about the world.

If Housel’s book has inspired you to start planning your finances better, trust ClickUp to simplify the game for you. This versatile project management and collaboration tool has many features to help you with finance planning and budgeting.

A cloud-based business management software, ClickUp can simplify your financial processes. Handle multiple accounts, generate easily shareable reports, and use ClickUp AI as your virtual personal assistant while you focus on the bigger picture.

Create custom Dashboards within ClickUp and build a digital map of your financial journey. Craft high-level proposals and reports showcasing budget allocations, actual spending, and profits, and get a comprehensive view of where, when, and how your money is flowing.

If you don’t enjoy number-crunching, use ClickUp AI, which is powered by natural language processing. It can turn numerical data into actionable insights for more thoughtful decisions.

Meanwhile, deadlines are easier to handle with ClickUp Tasks. It’s like setting personal financial reminders; invest and mark it done. It helps you build an effortless cycle that mirrors Housel’s idea of small, consistent actions for financial success.

But is that all? Nope.

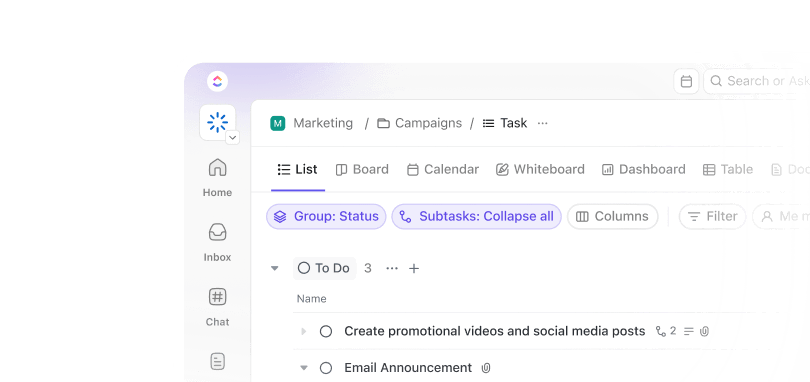

ClickUp comes with many templates designed just for budgeting and financial planning. For example, ClickUp’s Simple Budget template lets you track your monthly income and expenses.

With 16 custom fields and 5 views, including Budget Plan and Net Cash, this template helps you monitor and visualize your budget progress. It also boasts customizable statuses and project management features like time tracking, priority labels, dependency warnings, and emails.

ClickUp helps you take the grunt work out of managing money.

With bite-sized chapters, charts, and personal stories, The Psychology of Money introduces you to the power of healthy money habits like saving money and making smarter financial decisions. .

Take your financial planning up a notch with ClickUp. Organize and visualize your budgets and finances with the help of dashboards, recurring tasks, custom statuses, views, and more.

Make smart decisions, set your money-saving goals, and track your financial outcomes with ClickUp.

Sign up for ClickUp today for free and begin your journey to being wealthy.

Alex York

Max 11min read

Sudarshan Somanathan

Max 11min read

Sudarshan Somanathan

Max 12min read

© 2026 ClickUp